Shell Net Pension Scheme

The Shell Net Pension Scheme enables you to accrue a pension on the part of your salary above the statutory tax limit for your scheme. The government has set a tax limit for how much pension may be accrued from an employee’s gross salary. Above this limit, only net income (after income tax) can be saved towards a pension. For this purpose, Shell Pension has set up the Shell Net Pension Scheme. You can see how this works below.

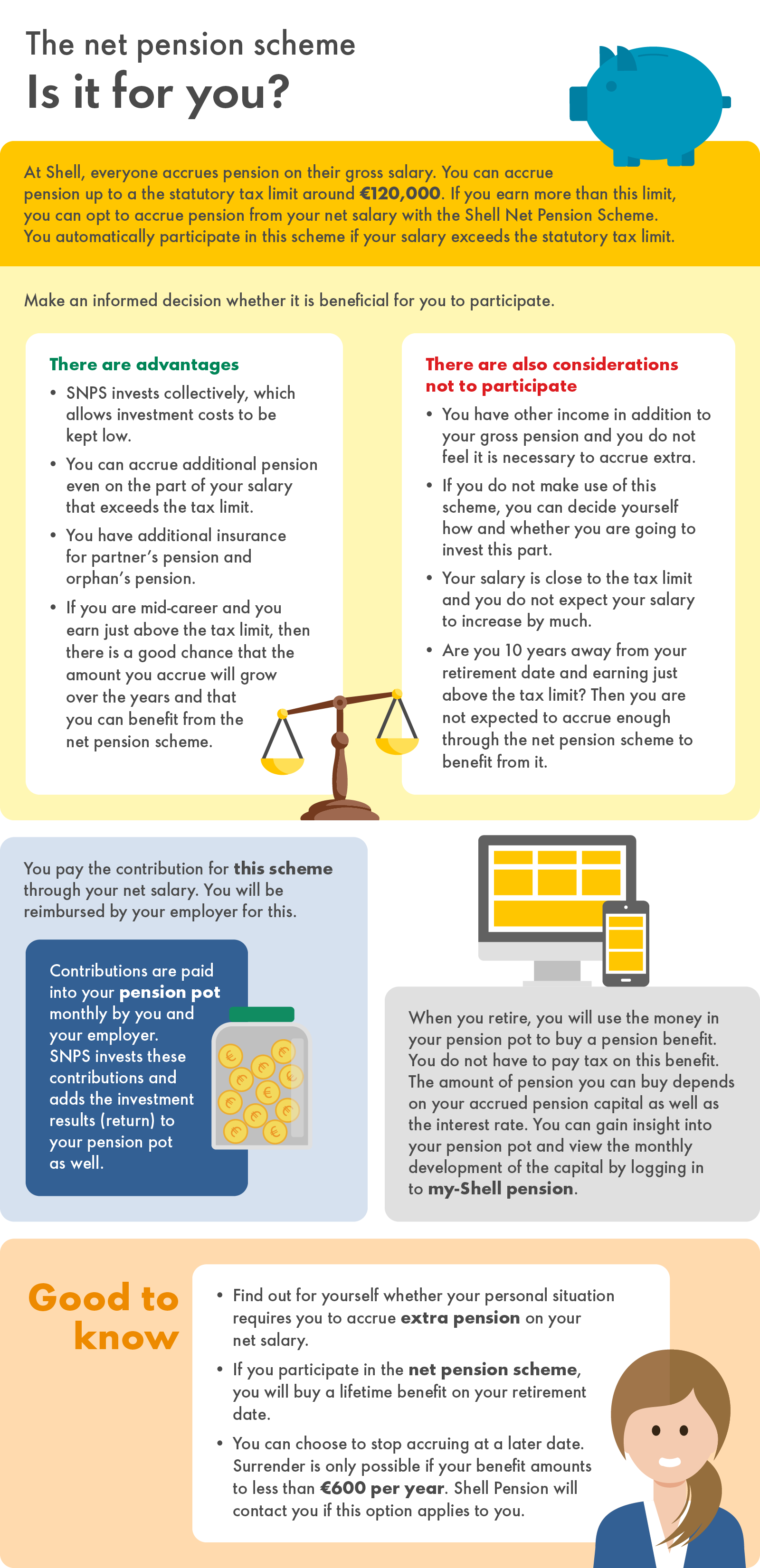

The tax limit for participating in the Shell Net Pension Scheme is approximately €120,000. In Pension 1-2-3, you can find the exact amount of the tax limit for participants of the Shell Pension Fund Foundation (SSPF) and for participants of the Shell Netherlands Pension Fund Foundation (SNPS). You can find all the agreements concerning your pension in the SNPS Pension Regulations for the Net Pension Scheme (pdf). The scheme works the same as the SNPS scheme of Shell Pension Fund Foundation. The Shell Net Pension Scheme allows you to accrue an old-age pension, partner's pension and orphan's pension and entitles you to a waiver of contributions in the event of (partial) occupational disability (PVI). Your occupational disability pension is arranged for your entire salary in your basic SNPS or SSPF pension scheme.

You will be reimbursed by your employer for this. The maximum permitted contribution permitted is age-related. This contribution is used to accrue your own pension capital. You then use this to purchase pension benefits later. You do not have to pay income tax on the pension benefits starting from the date of retirement. The opposite situation applies for the SNPS and SSF basic pension schemes. In the SNPS and SSPF scheme, you do not pay income tax on the premiums, but you do pay income tax on the pension benefits.

On my-Shell pension, you can see how your pension capital is performing every month. You can also find information on the options offered by your Net Pension Scheme. In addition, you will receive a Uniform Pension Overview (UPO) once a year. This shows the sum you have accrued for your net pension capital. You can also view the UPO on my-Shell pension.

This involves the risk premiums for the following insurances:

· Insurance for further pension accrual in the event of occupational disability.

· Insurance in the event of death during your employment (partner's pension and orphan's pension).

Is your salary higher than the tax limit for your scheme? Then you automatically participate in the Shell Net Pension Scheme. You will be notified of this. Unlike your basic pension scheme up to the tax limit, participation in the Shell Net Pension Scheme is not compulsory.

|

Participating in the Shell Net Pension Scheme has a number of advantages: • Accruing capital in the Shell Net Pension Schemeis more advantageous than doing it yourself: - SNPS invests collectively and can therefore keep investment costs lower than they would be if you if you were to invest by yourself. • Dependants receive a good partner's pension and/or orphan's pension, including on the portion of your pensionable salary above the tax limit. You continue to accrue pension capital on the portion of your salary above the tax limit, even if you are unable to work, or can no longer work, due to full or partial occupational disability. • Immediate participation is not subject to any medical examination. • You can cancel your Net Pension Scheme at any time. You can also resume participation one year after you have stopped. |

Considerations for opting out of participation in the Shell Net Pension Scheme: • You have other sources of income and do not find it necessary to accrue a net pension in addition to your gross pension • Your salary is close to the tax limit and you do not expect a significant salary increase. • If you choose not to pay into the Net Pension Scheme, but instead opt to have the contribution paid out with your salary, you have the freedom to do so. |

|

Prefer not to participate in the Shell Net Pension Scheme? Please let us know You can decide to opt-in again if you have opted out in the past

MEDISCH GEHEIM Once your health declaration has been approved, complete the Opt-in form. You will find this form at the bottom of the Downloads page. Send it to HR Operations via HR Online. Please add the approval received from the reinsurer to your application. |

In the e-learning Pension at Shell you will find information about the SNPS scheme. The Shell Net Pension Scheme is also discussed here.